Since information on your receipts can sometimes be used to access your accounts or harass you, you may wish to shred many of them. If you don't want to shred every receipt you get, take a look at what information is on a receipt to decide whether it's worth shredding. Remember that you may wish to hold on to some receipts for a while for tax or business recordkeeping purposes.

Documents to Shred

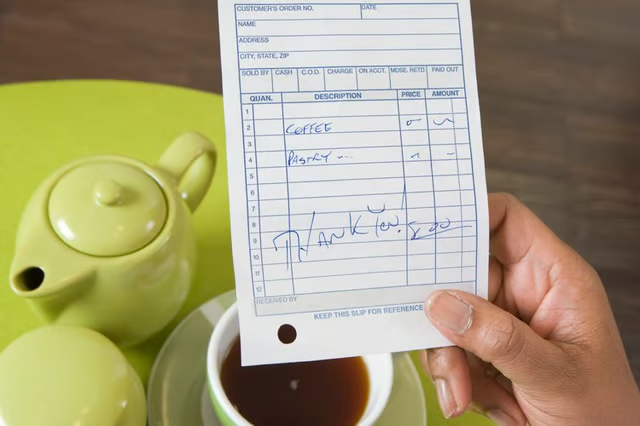

Under federal law, credit and debit card receipts aren't supposed to contain your full credit card number, only the last few digits. That makes it harder for thieves to use them to steal money from your account or impersonate you, but it's not impossible for them to still do so, since some companies do use those digits to help verify that you are who you claim to be. In general, you'll want to shred receipts with the last four digits or any other portion of your credit or debit card number on them, which is probably most card receipts you get.

You'll also generally want to shred receipts with other account numbers on them, such as receipts you might get for depositing a check with a bank teller, using an ATM, paying a utility bill or similar transactions. In some cases, you might want to shred any receipts with your name, address, phone number or email address on them, especially if those aren't pieces of information you widely make public.

You should also shred information you receive in the mail with account numbers on them or information that could be used to open accounts in your name. Shred credit card offers, for example, and offers for home equity loans and invitations to open bank accounts. Crosscut shredders, which disassemble paper into tiny pieces that are difficult to assemble, are considered the most secure.

If you have a receipt that doesn't have any personally identifiable information on it and isn't linked to any purchase you feel sensitive about, such as a cash receipt for a cup of coffee or a small grocery item, you're generally safe to simply discard it.

When to Hold On to Documents

If you're concerned about identity fraud, it can be tempting to shred every document as soon as you can, from old bank statements to gas station receipts. While you can safely shred credit card offers you're not going to use or other junk mail right away, there are some documents you'll want to keep.

While government documents like your Social Security card, birth certificate, car title and similar papers can be a boon to fraudsters, they're also often necessary, so you want to save them in a safe place, not shred them.

Similarly, even receipts can be worth holding on to for a while before you destroy them. Credit card receipts can be worth holding on to for a few months, in case you are dissatisfied with the transaction and need to contest it with your credit card company. Other receipts may be worth retaining if you think you might need to return the purchased item, invoke a warranty or claim a mail-in rebate.

For tax purposes, you generally want to keep receipts or other records for business and other deductions for at least three years, in case you are audited by the IRS. If you work for a company that requires receipts to get reimbursed for business expenses, check to see if your employer has a receipt retention policy you should follow.